A fight taking place in the WTO shows how the rules on agriculture allow rich countries to continue huge subsidies whilst penalising developing countries’ farmers.

By Martin Khor

Food is one of the most important and emotive of all issues. As consumers, we can’t survive without it.

Agriculture also employs the most people in most developing countries. Ensuring farmers have enough income is key to development and social stability.

Some countries that did not achieve this have faced first rural disgruntlement and then upheaval.

Increasing food self-reliance is a goal in many countries. Food security became a high priority after global food prices shot up to record highs in 2008, and there was a near-scramble for supplies of some food items including rice because of potential shortages.

Also, reducing and eventually eliminating hunger worldwide is one of the key development goals adopted by governments at the United Nations.

Against this background, there is a remarkable discussion now taking place at the World Trade Organization, as part of preparations for its Ministerial Conference in Bali in December.

Developing countries grouped under the G33 are asking that their governments be allowed to buy food from their farmers, stock the food and distribute it to poor households, without this being limited by the WTO’s rules on agricultural subsidies.

However their proposal is facing resistance, mainly from some major developed countries, especially the United States, whose Ambassador told the WTO earlier this year that such a move would “create a massive new loophole for potentially unlimited trade-distorting subsidies”.

This clash is an outstanding example of how the agriculture rules of the WTO favour the rich countries whilst punishing the developing countries, including their poorest people.

It is well known that the greatest distortions in the trading system lie in agriculture. This is because the rich countries asked for and obtained a waiver in the 1950s from the liberalization rules of the GATT, the predecessor of the WTO.

They were allowed to give huge subsidies to their farm owners, some of who do not even carry out farm activities, and to have very high tariffs.

When the WTO was set up, it had a new agriculture agreement that basically allowed this high farm protection to continue. The rich countries were obliged only to reduce their “trade distorting subsidies” by 20% and could change the nature of their subsidies and put them into a “Green Box” containing subsidies that are termed “non trade-distorting or minimally trade-distorting.”

There is no limit to the Green Box subsidies. So the trick played by the rich countries has been to move most of their subsidies to the Green Box, including subsidies that are not directly linked to production, or that are tied to environmental protection. But studies have shown that the Green Box subsidies are in fact trade distorting as well.

With this shifting around, the rich world’s subsidies have been maintained or actually soared. WTO data show that the total domestic support of the United States grew from US$61 billion in 1995 (when the WTO started) to US$130 billion in 2010.

The European Union’s domestic support went down from 90 billion euro in 1995 to 75 billion euro in 2002 and then went up again to 90 billion in 2006 and 79 billion in 2009.

A broader measure of farm protection, known as total support estimate, shows the OECD countries’ agriculture subsidies soared from US$350 billion in 1996 to US$406 billion in 2011.

The effects of continuing rich-country subsidies have been devastating to developing countries. Food products selling at below production costs are still flooding into the poorer countries, often eating into the small farmers’ incomes and livelihoods.

Ironically the developing countries, already the victims of the rich world’s subsidies, are themselves not allowed to have the same huge subsidies, even if they can afford it.

The reason is that the agriculture rules say that all countries have to cut their distorting subsidies. So if a developing country has not given subsidies before, they are not allowed to give any, except for a small minimal amount (10 per cent of total production value).

In other words, if you have given $100 billion subsidy, you have to bring it down to $80 billion and you can transfer the rest to the Green Box, but if you haven’t given any before, you cannot give one dollar, except for the minimum allowed.

This is where the present WTO controversy comes in. The developing countries are asking that food bought from poor farmers and given to poor consumers should be considered part of the Green Box without conditions.

The present rule sets an unfair condition: that any subsidy element in this purchase scheme should be considered a trade-distorting subsidy which for most developing countries is limited to this minimum amount (10% of production value).

Other Green Box subsidies, that developed countries mostly use, do not carry such a condition.

The developing countries merely seek to remove the unfair condition that in effect prevents them from adequately helping their poor to get sufficient food.

For example, India’s parliament has just passed a food bill that entitles the poor (two thirds of the population) to obtain food from a government scheme that buys the food from small farmers.

But the estimated US$20 billion-plus the government will spend annually may exceed the small minimum amount of subsidy it is allowed, because India was not a big subsidiser before the WTO rules came into force.

Other developing countries that provide subsidies to their farmers and consumers, such as China, Indonesia, Thailand, and Malaysia, may also one day find themselves the targets of complaints.

For rich countries who are subsidising a total of US$407 billion a year to disallow poor countries from subsidising their small farmers and poor consumers, is really a specially bad form of discrimination and hypocrisy. An outstanding case of the pot calling the kettle black!

Whether this controversy can be settled fairly before the WTO’s Bali Ministerial remains to be seen.

Comments Off on When Foreign Investors Sue the State

The investor-state dispute system, whereby foreign investors can sue the government in an international tribunal, is one of the issues being negotiated in the Trans-Pacific Partnership Agreement.

By Martin Khor

In the recent public debate surrounding the Trans Pacific Partnership Agreement (TPPA), an issue that seems to stand out is the investor-state dispute settlement system (ISDS).

It enables foreign investors of TPPA countries to directly sue the host government in an international tribunal.

In most US free trade agreements, the tribunal most mentioned is ICSID, an arbitration court hosted by the World Bank in Washington.

The ISDS is a powerful system for enforcing the TPPA’s rules. Any foreign investor from TPPA countries can take up a case claiming that the government has not met its relevant TPPA obligations.

If the claim succeeds, the tribunal could award the investor financial compensation for the claimed losses. If the payment is not made, the award can potentially be enforced through the seizure of assets of the government that has been sued, or through tariffs raised on the country’s exports.

The ISDS is related to relevant parts of the TPPA’s investment chapter. One of the provisions is a broad definition of “investment” which includes credit; contracts; intellectual property rights (IPRs); and expectations of future gains and profits. Investors can make claims on losses to these assets.

Under the national treatment provision, foreign investors can claim to be discriminated against if the local is given preference or other advantage.

Under the clause on fair and equitable treatment, investors have sued on the ground of non-renewal or change in terms of license or contract; and changes in policies or regulations that the investor claims will reduce its future profits.

Finally, investors can sue on the ground of “indirect expropriation”. Tribunals have ruled in favour of investors that claimed losses due to government policies or regulations, such as tighter health and environmental regulations.

The arbitration system has come under heavy criticism, including that the tribunal decisions are arbitrary and can contradict decisions of other tribunals in similar cases.

There is often a conflict of interest situation. A few lawyers monopolise the international investment arbitration business; they act as lawyers in one case and as arbitrators in other cases. In a few cases, an arbitrator was on the Board of Directors of the parent company of the investor that took up the case.

There is a pro-investor bias in many cases, with decisions or arguments that are quite clearly unfair to the governments being sued. However there is no appeal possible.

Another issue is the high awards and the strong enforcement, including seizure of assets.

The claims have tended to be very high in recent years, running to billions of US dollars. Awards are usually lower, but recent ones can also be very high, for example the US$2.3 billion award granted to an American oil company against Ecuador.

The ability to enforce these awards through seizure of assets owned and located abroad by the government makes the ISDS a very powerful instrument.

Among recent cases was an award by ICSID to a US oil company against Ecuador for US$2.3 billion; a case taken against South Africa by a European mining company claiming losses from the government’s black empowerment programme and a US$2 billion claim against Indonesia by a UK-based oil company, after its contract was cancelled because it was not in line with the law.

Australia has also been sued for billions of dollars by the tobacco company Philip Morris because of its regulation that the cigarette boxes cannot promote the logo and brand names.

An American company Renco sued Peru for $800 million because its contract was not extended after the company’s operations caused massive environmental and health damage.

There are several implications of the ISDS. Not conforming to TPPA rules can carry a heavy penalty, since government can be sued in an international court, and thus government will be constrained when formulating future policies or implementing existing ones.

It is difficult for government to make new policies, as it cannot predict whether certain policies it wishes to introduce or change is allowable, since it is uncertain or unpredictable how a tribunal will view this, i.e. the view of a particular tribunal can differ from that of another tribunal.

The country’s judicial sovereignty will be affected. Investors will choose to take up cases in the international tribunal where their chances of success and the pay-out are higher than in local courts.

The country will become vulnerable to multi million-dollar and billion-dollar legal suits taken by foreign investors. Potentially this may cost government a lot of financial resources.

The TPPA negotiations are still going on, and thus the ISDS component can still be negotiated. However, there is probably limited room for negotiation on the key aspects, since the USA is unlikely to deviate from the main points in its FTAs.

If the ISDS is deemed to contain too many problems, one option is to ask for an exception, i.e. that it does not apply to the country, similar to what Australia has requested. It is doubtful however whether such a request will be granted by other TPPA countries.

Martin Khor is Executive Director of the South Centre; contact at: director@southcentre.int.

Comments Off on New Threat to Economic Role of the State

The economically successful developing countries like Malaysia are characterised as having a strong “developmental state”. But this role of the state is coming under attack in new global rules being created.

By Martin Khor

Two new trade agreements involving the two economic giants, the United States and European Union, are leading a charge against the role of the state in the economy in developing countries.

Attention should be paid to this initiative as it has serious repercussions on the future development plans and prospects of the developing countries.

The role of the state, or of government, in development is a subject of long-standing and important discussion.

In fact some economists and analysts consider it perhaps the most important issue that determines the difference between economic success or failure in developing countries.

The immediate post-colonial period saw a tendency to a strong state, including government ownership of some key sectors, including industry and banking.

Past decades have witnessed a wave of privatisation across both rich and developing countries. But the state still owns or controls utilities, infrastructure, public services, banks and a few strategic industries in many developing countries.

State enterprises or commercially run companies owned by or partially linked to the government play an important role in many a developing country.

Private companies also receive state assistance and support in many ways, including loans to small and medium enterprises and farmers, subsidies and tax breaks for research and development or technology purchase, preferences in government procurement, infrastructure provision including in special economic zones.

Countries provide incentives for foreign companies, such as tax-free status. However, the state also has special treatment for local companies, such as grants, cheaper than normal credit and subsidies, and government contracts.

The developmental role of the state in developing countries is now coming under attack from developed countries.

This is promoted by the big companies in the US, Europe and Japan, which seek to enter the markets of developing countries which are the source of their future profits.

The support given by the state to domestic companies are seen by the multinational companies as a hindrance to their quest for expanded market share in developing countries.

They are thus seeking to change the worldview and policy framework in developing countries, to get them to reduce the role of state enterprises as well as to curb the government’s promotion of local private companies.

The two latest big attempts towards this is through the Trans-Pacific Partnership Agreement (TPPA) and the Trans-Atlantic Trade and Investment Partnership (TTIP).

A sub-chapter on state-owned enterprises (SOEs) is a prominent part of the TPPA, which was negotiated in Kota Kinabalu that fortnight.

The United States and Australia are leading the move to have rules to discipline the role of the government in the economy, through a two prong approach. First, to get government or other monopolies to behave in a “non-discriminatory” way, including when they buy or sell goods and services. This includes that they may not give preferences or incentives to the local firms.

Second, companies that are linked to the government (including through a minority share) should not get advantages vis-à-vis other firms in commercial activities. Of course the developed countries that are proposing this are thinking of their companies – how they can get more access to developing countries’ markets.

In the TTIP, a US-European Union agreement, negotiations for which started earlier in July, the European Union is preparing a sub-chapter on state owned enterprises, with rules that seem quite similar to what the US and Australia are proposing in the TPPA.

Although the TTIP only involves Europe and the US directly, the rules it sets are intended to have consequences for other countries.

According to press reports, the two economic giants are planning that the rules they set in the TTIP will become the standard or template for future bilateral agreements that also include developing countries.

They also hope that these rules will be internationalised in the World Trade Organization, which has over 130 member states.

The EU’s position paper on SOEs says that its aim is to “create an ambitious and comprehensive standard to discipline state involvement and influence in private and public enterprises”.

And that “this can pave the way to other bilateral agreements to follow a similar approach and eventually contribute to a future multilateral engagement.”

In other words, the constraints on the role of the state, and the reduction of the space for behaviour or operations of state-linked companies, will become the way of the future for all countries, if the US and European plans succeed.

What is moving these countries in this direction? It is quite well known that the negotiating positions of the developed countries are greatly influenced and in fact driven by their big companies.

Their trade policy makers and negotiators usually act on behalf of these companies.

Reports by the specialist trade bulletin Inside US Trade show how corporate groups like the US Chamber of Commerce and the Coalition of Services Industries have been pushing for the new rules on state owned enterprises, and also how they are targeting to open up the markets of developing countries especially China.

These attempts to curb the role of the state in the economy are worthy of serious study and counter-action.

Developing countries that succeeded in economic development were able to combine the roles of the public and private sectors in a partnership that advanced overall national development.

Asian countries, including Japan, South Korea, Malaysia, Singapore, and China, have pioneered this model of public sector collaboration with the private sector.

Those few developing countries that managed to get development going were all driven by the “developmental state”, or the leadership role of government in establishing the framework of economic strategy, and the collaboration between the state, state enterprises, and commercial companies, including those in which the state has an interest.

If developing countries like Malaysia have to come under new international rules that curb the role of the state and that re-shape the structure of their economy, then the prospects for future development will be adversely affected.

Comments Off on Where Next for Developing Countries? – Future Prospects and Risks for South’s Economies

Despite adverse fallouts from the most severe post-war economic crisis and downturn in advanced economies (AEs), on average, developing countries (DCs) have so far managed to sustain an acceptable pace of economic growth for the reasons discussed above. Compared to the beginning of the crisis, total income in the developing world is now higher by almost one-third whereas AEs have barely managed to maintain their pre-crisis levels of income. Although growth in many major DCs is now considerably slower than the rates achieved before the onset of the crisis, there are widespread expectations, notably among policy makers, that prospects are brighter in the coming years, once the worst post-war crisis is fully overcome, economic activity is stabilized and employment and output gaps are reduced in AEs. These would allow DCs to go back to catch-up growth and continue to converge towards income levels of AEs, very much as in the period before the onset of the crisis.

There are, however, important question marks regarding these expectations. First, it is not clear when the crisis will be over and if DCs can sustain a reasonable pace of growth in the event of protracted instability and weakness in AEs. There are still serious downside risks, notably from the Eurozone (EZ) and China, and global economic conditions could worsen before starting to improve. Second, the exit of AEs from the crisis may not necessarily improve global economic environment in all areas that affect the performance of DCs. AEs may not be able to move to a high and stable growth path and global financial conditions may tighten considerably with their exit from the ultra-easy monetary policy. Third, growth prospects of most DCs also depend crucially on China. Although China has withstood severe fallouts from the crisis, there is considerable uncertainty whether it can maintain strong growth over the longer term.

Downside risks

No doubt the EZ is now the Achilles’ heel of the global economy and the immediate threat to stability and growth in DCs. Although financial stress in the region has declined considerably, adjustment fatigue or political turmoil in the periphery could still deepen the crisis and even lead to a total break up. However, it is difficult not only to predict the evolution of the EZ in the coming years, but also the impact of a break-up, since past economic and financial linkages would provide little guide for estimating the consequences of such an unprecedented event. Still, even without a total break-up, an intensification of financial stress could have serious repercussions for DCs, as suggested by various downside scenarios simulated by the IMF, the UN and the Organisation for Economic Co-operation and Development (OECD).

Financial contagion to DCs from a major turmoil in the EZ, notably a default and exit, could be much more serious than adverse spillovers through trade because it would affect balance sheets and be more difficult to handle with standard macroeconomic policy tools. The main channel would be capital flows, asset prices and exchange rates, which have already become highly sensitive to news from the EZ, as noted. The impact could be similar to that triggered by the collapse of Lehman brothers in 2008 – a flight to safety, stronger dollar and sharp declines in assets and currencies in DCs. It could be longer lasting than Lehman, because of difficulties in restoring confidence and stability.

The outlook of the global economy is also clouded by downside risks surrounding China. It has been increasingly argued, including by a prominent Asian investment bank, Nomura Holdings Inc., that because of the credit and property bubbles created by its response to fallouts from the crisis, China now displays the symptoms that the US showed before the sub-prime crisis. On this view, if a loose policy stance is maintained and the risks are not brought under control, strong growth above 8 per cent could be attained in 2013, but only to be followed by a financial crisis as early as 2014 (Wall Street Journal, 2013; Frost, 2013). Again, a global survey of fund managers conducted in March 2013 has shown widespread expectations of a hard landing in China (Emerging Markets, 2013). The loss of growth momentum in the first quarter of 2013 has also renewed fears of an imminent crisis in the banking system.

The impact of a financial turbulence in China on DCs could be more serious than that of a sharply increased financial stress in the EZ. It can be expected to lead to a sudden reversal of capital inflows, a sharp correction in asset markets and strong downward pressures on the currencies in the developing world. Such adverse financial spillovers would be aggravated by the impact of a sharp drop in China’s demand for commodities. Consequently, DCs heavily dependent on capital flows and commodity exports are particularly vulnerable to a financial turbulence and a hard landing in China.

However, a severe financial stress in China does not have a high probability of occurrence. As argued by Anderlini (2013), even if the risks are not (or could not be) immediately brought under control, in China “a Lehman style collapse is impossible” and its “banking system is more likely to undergo slow erosion” because of extensive state ownership and guidance.

Longer-term prospects

In considering the longer-term prospects for the global economy, the prospects for the US and Europe are of course crucial. This has already been analysed in the pervious issue of the South Bulletin. We now consider the situations of China.

The response of China to fallouts from the crisis has served to rebalance domestic and external demand, but aggravated the imbalance between investment and consumption, which had already been building up in the period before the crisis. Investment has been the main driver of growth since 2009 and consumption has been growing only marginally faster than income. However, China cannot keep on pushing investment to fill the deflationary gap created by the slowdown in exports in conditions of exceptionally low shares of wages and household income in GDP. That would add more to financial fragility and imbalances than to productive capacity and potential growth. Nor can it go back to export-led growth and constantly increase its penetration of foreign markets. This would be resisted, possibly causing disruptions in the trading system.

Regardless of how the existing financial fragilities created by the credit and investment bubbles are handled, the most likely medium-term scenario for China is a sizeable drop in its trend growth compared to double-digit rates it enjoyed in the run-up to the crisis, with a better balance between domestic and external demand and a gradual rebalancing of domestic consumption and investment. Indeed, research conducted at the Chinese Development Research Centre on growth prospects of China is reported to have concluded that, for a number of reasons on the demand and supply sides, such a transition to slower growth is already under way and the growth rate is expected to come down to 6.5 per cent during 2018-22 after three decades of double-digit levels (Wolf, 2013). However, the possibility that China may also get caught in a middle-income trap is not excluded (Bertoldi and Melander, 2013; ADB, 2011).

The transition of China to a lower growth path over the next few years implies that its demand for commodities would grow much more slowly than in the past decade. This would result not only from slower growth but also rebalancing of demand towards consumption, which is much less import intensive than either exports or investment (Akyüz, 2011a). Improvements in the efficiency in the use of materials could also reduce the pace of China’s demand for materials (UNEP, 2013). Together with a stronger dollar, these could imply significant loss of momentum in commodity prices, short-circuiting the commodity super-cycle and lowering its mean in conformity with the observed historical pattern (Erten and Ocampo, 2012).

Nor can China be expected to become a locomotive for exporters of manufactures in the developing world. Its imports of manufactures from DCs have so far been destined mainly for exports rather than for domestic consumption which has very low import content (Akyüz, 2011a). A more balanced growth between exports and domestic consumption would imply slower growth of imports of parts and components from other DCs. On the other hand, there is still some time before China could exit from labour-intensive, low-skill manufactures and become a major market for lesser developed countries in these products, relocating such industries, à la Flying Geese, in lower-cost countries in South and South East Asia and Africa.

Conclusions

The crisis in AEs has aggravated the problem of underconsumption that the world economy has been facing due to low and declining share of wages in income and increased concentration of wealth. Rising inequality is no longer only a social problem. It has also become a serious macroeconomic problem, compromising the ability of the world economy to achieve strong and sustained growth and financial stability. The solution calls for strong action on its causes – financialization, the retrenchment of welfare state and globalization of production. However, the likelihood of fundamental changes in these areas is slim. Thus, the post-crisis world economy may either go back to finance-driven boom-bust cycles, enjoying unsustainable expansions followed by deep and prolonged crises, or may have to settle at a slow growth path. It is against this background that DCs need to rethink their development policies.

Not only has the “Great Recession” led to a “Great Slowdown” in DCs (Economist, 2012), pushing growth rates possibly below stalling speeds in some, but also medium-term prospects for global economic conditions look unfavourable compared to pre-crisis years and, in some respects, even compared to the period since the onset of the crisis. Thus the rapid rise of the South that began in the early years of the new millennium appears to have come to an end. This should not come as a surprise since, as argued in Akyüz (2012), the exceptional performance of DCs in the run up to the crisis was driven primarily by exceptional global conditions. There were little signs of tangible improvements in the underlying growth fundamentals or dynamics in DCs experiencing acceleration.

That acceleration took place without any significant progress in industrialization without which most DCs cannot converge and graduate to the levels of productivity and living standards of AEs. Of the so-called BRICS (Brazil, Russia, India, China and South Africa), only China promises sustained catch-up growth and graduation even though it faces a bumpy road. Brazil, Russia and South Africa continue to depend heavily on commodities and have indeed deepened their dependence by expanding the commodity sector relative to industry. The two key determinants of growth in Latin America and Africa, commodity prices and capital flows, are largely beyond national control and susceptible to sharp and unexpected swings. At a bare 3 per cent, the average potential growth rate of Latin America is far too low, even if constantly realized, to close the income gap with AEs. Many second-tier Newly Industrializing Economies (NIEs) in Asia seem to be caught in the middle-income trap, facing growing competition from below without being able to upgrade and join those above – the first-tier NIEs and Japan. India has been relying on the supply of labour to the rest of the world, not by converting them into higher-value manufactures, but by exporting unskilled workers and IT and other labour services of a very small proportion of its total labour force (Nabar-Bhaduri and Vernengo, 2012).

As one development practitioner has put it, for DCs it would now be “unwise to count on tail winds; they will likely weaken, become more volatile, or both” (Torre, 2013). The remarkable performance of most DCs in the past decade is in danger of remaining a “one-off success” unless they raise productive investment, accelerate productivity growth and make significant progress in industrialization. Globalization has been oversold to DCs. They have largely left their development to international market forces shaped mainly by policies in AEs and their financial conglomerates and transnational corporations in control of international production chains.

Despite growing disillusionment in the South, the Washington Consensus is dead only in rhetoric. There is little roll back of policies pursued and institutions created on the basis of that consensus in the past two decades. On the contrary, the role and impact of global market forces in the development of DCs has been greatly enhanced by continued liberalization of trade, investment and finance unilaterally or through bilateral investment treaties and free trade agreements with AEs. DCs need to be as selective about globalization as AEs, and reconsider their integration into the global economic system, in recognition that successful industrialization is associated neither with autarky nor with full integration, but strategic integration designed to use foreign markets, technology and finance to pursue industrial development.

This implies rebalancing external and domestic forces of growth and development. Since the end of the so-called import-substitution, inward-oriented policies, the pendulum has swung too far. Dependence on foreign markets and capital should be reduced. There is also a need to redefine the role of the state and markets, not only in finance but also in all key areas affecting industrialization and development, keeping in mind that there is no industrialization without active policy.

Comments Off on Impact of Global Crisis on Trade and Trade Imbalances

International trade has been the single most important channel of transmission of contractionary impulses from the financial crisis and recession in the US and the EU. After growing at an average rate of some 7 per cent per annum, the volume of imports by Advanced Economies (AEs) first decelerated sharply in 2008 and then fell by 12 per cent in 2009, largely because of the decline in imports by the US. It bounced back in 2010 due to a broad-based recovery, but lost momentum as Europe went into tailspin. Growth of total volume of imports by AEs barely reached 1 per cent in 2012. In order to avoid a sharp deceleration of growth, Developing Countries (DCs) have had to rely on their own markets or South-South trade. In fact, given the widespread economic downturn in AEs, the latter have also sought expansion in developing country markets in order to kick-start recovery.

While all DCs have been hit directly or indirectly by the contraction and slowdown in imports by AEs, the incidence varied from country to country according to their dependence on exports, the relative importance of markets in AEs and the import content of their exports. In countries with very high ratio of exports to GDP, particularly in exporters of manufactures, import content of exports also tends to be high. Thus, any decline in exports entails cuts, pari passu, in imports used directly and indirectly for exports. Declines in exports also reduce imports through their impact on income and domestic demand, including imports from all countries. Indeed, as a result of these cumulative effects, in volume terms the world trade declined at much the same rate as the rate of decline of volume of imports by AEs. The decline in dollar terms was almost twice as large because of a sharp decline in prices, particularly for commodities.

On some estimates, trade shocks incurred by developing countries in 2009 as a result of the crisis amounted to 4.4 per cent of their GDP, of which 3.3 per cent was due to demand shocks resulting from declines in export volumes and the rest was the terms of trade shock resulting from price changes (UN WESP, 2010). Among the regions the total shock was greatest, over 12 per cent of GDP, in West Asia because of a sharp drop in oil prices, followed by Africa (5.5 per cent), East and South Asia (3.3 per cent) and Latin America and the Caribbean (2.3 per cent).

Among major DCs, the trade impact of the crisis has been particularly severe for China because of its dependence on exports to AEs. In the period 2002-07, Chinese exports grew by more than 25 per cent per annum, accounting for about one-third of GDP growth, taking into account their import contents. The dependence on exports to AEs was even higher for smaller exporters of manufactures in Asia, both directly and through supplying parts and components to China. With the outbreak of crisis in AEs, exports of Asian DCs first slowed sharply in 2008 and then dropped in 2009, and became a major drag on activity, reducing growth by 5-6 percentage points (Akyüz, 2012).

Import cuts in Europe have hit Africa and Central and Eastern Europe particularly hard because of strong trade linkages; more than 50 per cent of exports of several non-EU European countries and some North African countries are destined to the EU and the figure is over 35 per cent for several countries in sub-Saharan Africa as well as Russia (IMF, 2011). The direct effects of cuts in exports to the EZ during 2011-12 are estimated to have reduced growth by some 0.8 per cent in South Africa and Russia, 0.5 per cent in China and India, and 0.3 per cent in Brazil and Indonesia (OECD 2012: Box 1.1.). Many DCs in sub-Saharan Africa relying heavily on exports to Europe were also hit hard. These include Côte d’Ivoire, Mozambique and Nigeria where exports to the EU account for between 10 and 17 per cent of GDP (Massa et al., 2012).

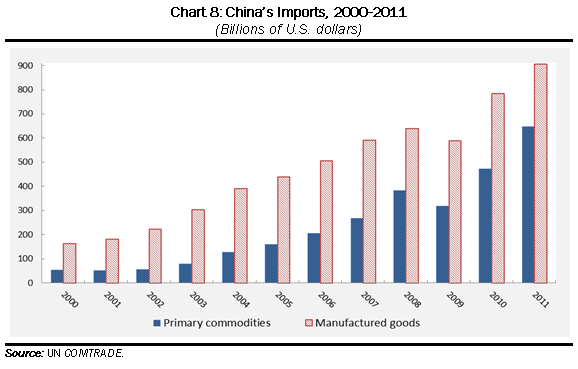

The crisis has resulted in significant changes in the pattern of world trade. Before the crisis South-South trade was largely conditioned by trade between DCs and AEs. China’s imports of manufactures from Asian DCs and commodities from all developing regions accounted for a large proportion of South-South trade and were mainly used, directly or indirectly, for its exports of manufactures to AEs (Akyüz, 2011a, 2012). With the shift of China to investment-led growth, not only has there been a shift in Chinese imports from manufactures to commodities (Chart 8), but also a larger proportion of imports have come to be used for domestic demand – over 55 per cent in 2011 compared to less than 50 per cent in 2007.

This has also meant that for many commodity exporters, China has become the single most important market. For instance, in 2007 Brazilian exports to the EU and US were four times and twice the level of its exports to China, respectively. Now the Brazilian exports to China and Europe are about the same and Brazilian exports to the US are one-half of its exports to China.

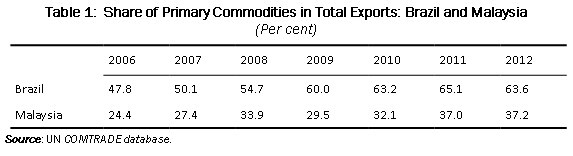

Furthermore, both because of the rise in commodity prices and the expansion of volume of exports, commodities have also come to account for an increasing proportion of exports of several semi-industrialized exporters of manufactures in the South. This includes not only Brazil but also some South East Asian DCs such as Malaysia. The increase in the share of primary commodities in total exports of these countries which had already started before the onset of the crisis has accelerated after 2009 (Table 1). In Brazil export earnings from commodities now exceed those from manufactures by a large margin. In Malaysia, widely considered as one of the successful second-tier Newly Industrializing Economies (NIEs), manufactures do not dominate export earnings if measured in value-added terms since they have much higher import contents than commodities. If account is taken of import contents, the share of manufactures in (value-added) exports would be about the same as, if not lower than, the share of primary commodities.

Trade imbalances

The crisis has resulted in a significant shift in global trade imbalances. With the increased reliance of DCs on domestic demand for growth, current account surpluses in export-led East Asia have declined while many other DCs have moved from surpluses to deficits or started to run larger deficits. On the eve of the crisis, DCs taken together had a current account surplus of almost $700 billion and a little more than one-half of this was due to China. It fell by almost $300 billion by the end of 2012 despite a $130 billion increase in the current account surplus of the Middle East and North Africa as a result of increases in oil revenues. The surplus of developing Asia fell from $400 billion to $130 billion, China from $350 billion to $210 billion while Latin America and sub-Saharan Africa both moved from surpluses to deficits.

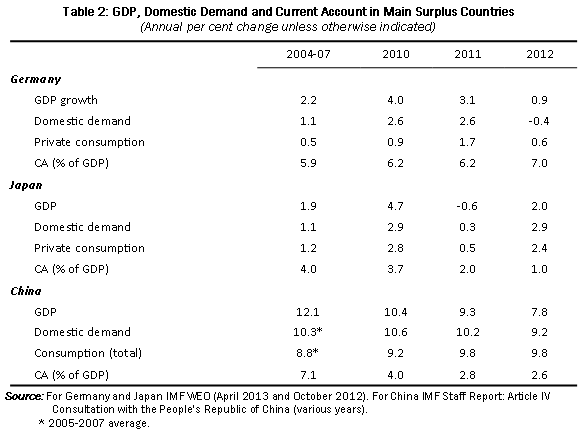

DCs have absorbed a large part of adjustment in global imbalances that had pervaded before the outbreak of the financial crisis. The current account deficits of AEs taken together fell from a peak of $480 billion in 2008 to less than $60 billion in 2012. The US current account deficit fell by $200 billion while the EZ moved from a deficit of $100 billion to a surplus of $220 billion. Of the three major surplus countries, the current account surplus of Germany has increased after the onset of the crisis, reaching 7 per cent of GDP at the end of 2012 (Table 2). Germany now runs trade surplus against China. By contrast, both Japanese and Chinese surpluses have fallen sharply. The decline in China’s surplus has been particularly dramatic, from a peak of 10 per cent of GDP in 2007 to 2.6 per cent in 2012.

As noted, in the run-up to the crisis the share of wages and private consumption in GDP was on a downward trend in all three major surplus economies, Germany, Japan and China. In all three countries GDP growth rates exceeded the growth rates of domestic demand. Growth was much slower in Germany and Japan but more dependent on exports than in China where imports expanded by double-digit rates thanks to a very strong growth of domestic demand (Akyüz, 2011b).

After the outbreak of the crisis, Germany has continued to rely on exports. Its GDP growth exceeded growth of domestic demand in every year throughout 2010-12, thereby sucking in foreign demand and effectively exporting unemployment. It has thus continued to be a major source of imbalance not only in the EZ, but also globally. By contrast, China has provided a major demand stimulus to the rest of the world by expanding domestic demand and allowing its real effective exchange rate to appreciate by some 20 per cent since the onset of the crisis.

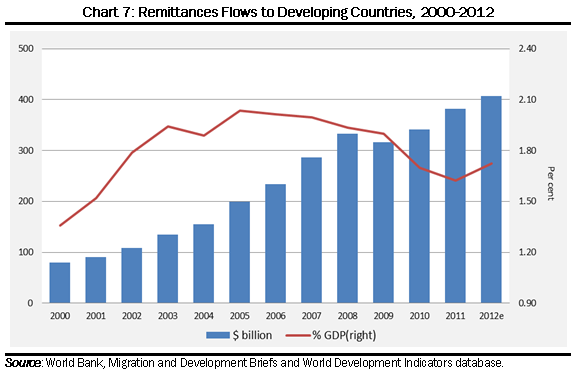

Worker’s remittances have emerged as a major source of external financing for Developing Countries (DCs) in the new millennium, second only to FDI inflows. They have followed broadly the same pattern as private capital inflows, expanding at a rate of 20 per cent per annum during 2002-08. They reached the peak of some 2 per cent of GDP of DCs taken together in the middle of the decade, mostly from migrant workers in the EU, followed by the US. For several DCs, they provided an important source of current account financing, at a rate of more than 3 per cent of GDP in India and Mexico and over 10 per cent in Bangladesh and the Philippines.

Surprisingly the crisis in the US and EU did not have a strong impact on total inflows of remittances to DCs even though these economies account for a very large proportion of total remittances and they have experienced sharp increases in unemployment after 2008. In nominal terms, remittances registered a small decline in 2009 followed by a moderate recovery afterwards, and are estimated to have reached $400 billion at the end of 2012. However, this has not been sufficient to reverse the decline in percentage of GDP of the recipient countries. At the end of 2012 they are estimated to have amounted to 1.7 per cent of GDP, compared to over 2 per cent during the pre-crisis peak (Chart 7).

Traditionally, remittances to DCs have generally served to support consumption of families and relatives in the countries of origin of migrant workers and financed mainly from their current earnings. However, existing statistical recording of these flows do not allow a precise determination either of the origin or of the final use of these transfers. They may actually be funded from accumulated savings of workers abroad and/or used in their countries of origin not for consumption but for investment in property or financial assets.

The continued increase in remittances to DCs after sharp rises in unemployment and declines in wages in the crisis-hit Advanced Economies (AEs) suggests that a greater proportion of these may have actually come from accumulated savings rather than current earnings of migrant workers. In the same vein, these might have been increasingly used for investment rather than consumption. In other words, they may be like capital flows rather than unrequited transfers. Increased rates of return on real and financial assets in DCs relative to AEs and the change of the risk perceptions against AEs may have encouraged such transfers. This has the implication that in the event of a shift in relative risk-return profiles of investments in AEs and DCs, these flows may well be reversed in the form of increased capital outflows from DCs.

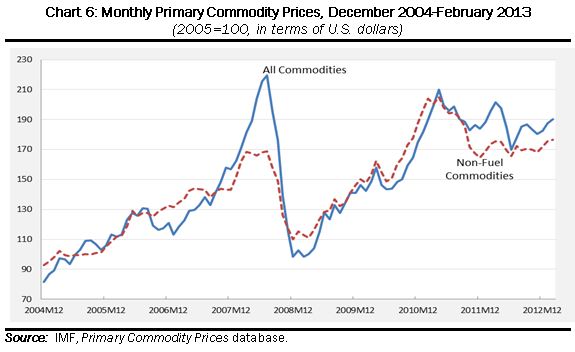

The financial crisis in Advanced Economies (AEs) has not depressed commodity prices to the extent seen in previous post-war recessions. The boom that had started in 2003 continued until summer 2008 with the index for all primary commodities rising by more than threefold (Chart 6). This was followed by a steep downturn in the second half of 2008, which took the index back to the level of 2004. But like capital flows and remittances, commodity prices also recovered strongly from the beginning of 2009, rising until spring 2011 when they levelled off and started to fall, manifesting increased short-term instability. In the early months of 2013, the index for all commodities was 15 per cent below the peak reached in summer 2008.

Different commodities that go into the aggregate index in Chart 6 are not only linked to economic activity in different ways, but have also important supply-side differences.Still, the behaviour of prices of commodity sub-categories has been broadly similar and highly correlated with global economic activity, particularly in Developing Countries (DCs), suggesting the dominance of common demand-side factors. Rapid growth in major commodity-importing DCs, notably China and to a lesser extent India, played a central role in the pre-crisis boom. Growth in commodity-dependent DCs also added to the momentum by creating demand for each other’s primary commodities. Prices increased along with the share of DCs in world commodity consumption. Oil demand from DCs is now as high as that from AEs, with China importing as much as the Eurozone (EZ) and twice as much as Japan. In metals, China alone accounts for more than 40 per cent of world demand.

The boom that started in 2003 and has generally continued except for a short-lived sharp downturn in 2008 is seen as the beginning of a new commodity super-cycle driven by rapid growth and urbanization in China (Farooki and Kaplinsky, 2011; Farooki, 2012). Historically such cycles are found to range between 30-40 years with amplitudes 20-40 per cent higher or lower than the long-run trend, with non-oil prices closely following world GDP (Erten and Ocampo, 2012).

After the outbreak of the financial crisis in AEs, the momentum in commodity prices has been kept up entirely by growth in the South, notably in China whose import composition changed rapidly from manufactures to commodities as a result of its shift from export-led to investment-led growth. As its markets in major AEs started to shrink in 2008, China introduced a large investment package, notably in infrastructure and property, pushing the ratio of investment to GDP towards 50 per cent. Since such investment is much more intensive in commodities, notably in metals, than exports of manufactures which rely heavily on imported parts and components from other East Asian economies, the shift from export-led to investment-led growth has led to a massive increase in Chinese primary commodity imports, which doubled between 2009 and 2011 compared to some 50 per cent increase in its manufactured imports (Chart 8). During the same period prices of metals rose by 2.4 fold, much faster than other primary commodities.

The downturn in commodity prices that started in 2011 has coincided with the slowdown in China and India. Given the credit and property bubbles and excessive debt and capacity generated by the 2008 stimulus package, China has been hesitant to respond to the slowdown with a similar package, allowing, instead, its growth to fall below 8 per cent for the first time for several years. The slowdown in China has been reflected particularly by a sharp decline in metal prices, by some 25 per cent between the beginning of 2011 and end of 2012, considerably steeper than declines in other commodities.

Because of increased financialization of commodities and growing interdependence between financial and commodity markets, the financial crisis has also generated considerable instability in commodity prices. The severe swings seen during 2008 had an important speculative component. Within the first 6 months of that year, the overall price index rose by some 35 per cent, followed by a sharp decline of 55 per cent in the second half of the year. No change in supply conditions or demand for physical commodities in such a short span of time can explain such a sharp swing. It was largely caused by rapid, self-reinforcing shifts in trading in commodity features triggered by rapid changes in expectations and sentiments around the collapse of Lehman Brothers, about the depth of the crisis and its possible impact on commodity prices.

Since 2011, the EZ crisis has had a strong influence on commodity prices not only by weighing on the demand from the region but also through financial channels. First, it has had a depressing effect on commodity prices by making the dollar stronger than it would have otherwise been. Second, it has added to commodity instability by triggering surges of entry and exits in markets for commodity derivatives. Like capital flows, commodity prices have become highly sensitive to news coming from the EZ.

The short-term outlook for commodity prices is highly uncertain not only because of possible supply-side disruptions, notably in energy and food, but also because of demand uncertainties. The latest projections by the IMF WEO (April 2013) are for continued declines in 2013-14 for both oil and non-fuel primary commodities. These are based on the assumption of no drastic change in conditions in two main economies strongly affecting commodity prices – China and the EZ. However, in both cases risks are on the downside, raising the possibility of steeper declines than is projected.

Comments Off on Financial Spillovers: Volatile Capital Flows and Currency Rates Cause Instability in the South

The financial crisis in Advanced Economies (AEs) has led to considerable instability of private capital inflows, yield spreads, equity prices and exchange rates in Developing Countries (DCs). The surge in capital inflows to DCs that had begun in the early years of the 2000s with sharp cuts in interest rates and rapid expansion of liquidity in AEs continued unabated in the early months of the crisis. However, the flight to safety triggered by the Lehman collapse led to a sudden stop and reversal, resulting in strong downward pressures on exchange rates and asset prices. Closer and deeper integration with major financial centres and rapidly growing gross asset and liabilities positions of DCs with the AEs intensified the transmission of financial stress to asset, banking and currency markets. The crisis also led to a contraction of credit in DCs due to cut-back in international bank lending and local lending by foreign banks’ affiliates in DCs as well as declines in inter-bank cross-border lending for funding by domestic banks (Cetorelli and Goldberg, 2010).

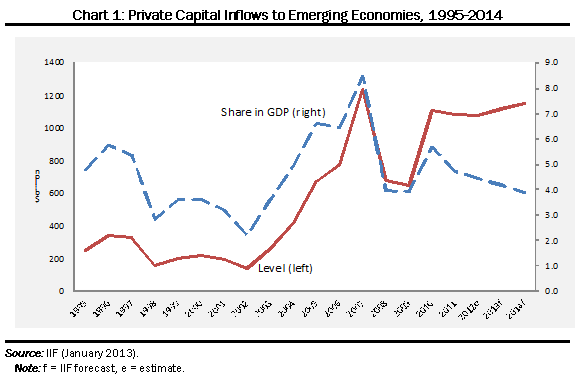

Although private capital inflows recovered quickly from early 2009, helped by sharp cuts in interest rates and quantitative easing (QE) in AEs and shifts in risk perceptions against them, they have lost their pre-crisis momentum and have become unstable and uneven. At the end of 2012, in nominal terms they were below the peak reached in 2007. As a percentage of GDP of the recipient countries, the decline was much steeper, from 8.5 per cent in 2007 to 4 per cent, a level not much different from those seen in the 1990s (Chart 1). Net flows available for current account financing and reserve accumulation in DCs are much lower, less than 1 per cent of GDP, because of resident outflows from DCs through direct and portfolio investment abroad. Institute of International Finance (IIF, January 2013) projections are for a moderate increase in 2013-14; but in absolute terms they are not expected to reach the 2007 peak and as a percentage of GDP they could continue to fall.

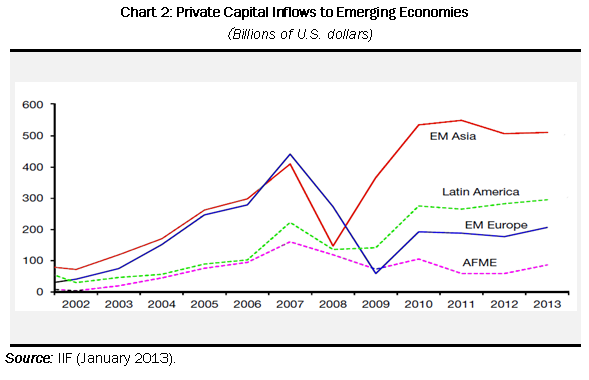

While the pre-Lehman boom in capital inflows was broad-based, pull factors have become more important in the post-Lehman recovery with lenders and investors increasingly differentiating among DCs. In absolute nominal terms net inflows to Asia and Latin America have exceeded the peaks reached on the eve of the global crisis even though the slowdown in China after 2010 has led to some deceleration in direct investment (Chart 2). By contrast, despite some recovery, inflows to European emerging economies have remained well below the peak reached before the crisis, largely due to strong fallouts from the Eurozone (EZ) crisis. This is also true for Africa and the Middle East.

The EZ crisis has played a central role in the overall weakness of private capital inflows to DCs. On the one hand, it has led to increased global risk aversion and greater preference for relatively safe assets. On the other hand, it has impinged directly on the volume of global capital flows. Before the outbreak of the global crisis, Europe was the main source of (gross) capital flows to the rest of the world, with $1600 billion per annum during 2004-07, higher than total outflows from the US and Japan taken together. With the outbreak of the crisis and the consequent bank deleveraging, total outflows from Europe fell sharply, registering a bare $300 billion a year during 2008-11.

The EZ crisis has also led to considerable short-term, month-to-month volatility in capital inflows to DCs as they have become increasingly sensitive to news coming from the region, leading to difficulties in macroeconomic management in DCs. From mid-2011, market sentiments turned sour with the deepening of the Greek crisis, strikes and political turmoil in the periphery and credit downgradings, leading to a drop in estimated capital inflows to DCs and significant downward revisions in forecasts.

Global risk appetite improved in the early months of 2012 with the agreement on European Stability Mechanism (ESM) and austerity packages in Greece and Spain, the implementation of the Long-Term Refinancing Operations (LTRO), the signing of the Fiscal Compact and increased lending limits from the European Financial Stability Facility (EFSF) and the ESM.

However, markets became bearish again after spring 2012 when Spain requested assistance for bank capitalization, was downgraded by rating agencies and its yield spreads mounted, and concerns grew over Greece. As already noted, this was followed by renewed optimism after mid-2012 with the commitment of the European Central Bank (ECB) to save the euro. However, the mood changed again with the confusion created by the Cypriot bailout plan in March 2013.

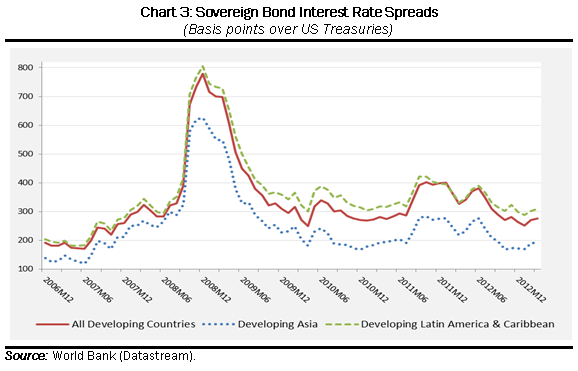

Changes in global risk appetite and private capital flows have also been mirrored by bond and equity markets of major emerging economies (Chart 3 and 4). After the Lehman collapse, sovereign bond spreads shot up and stood, at the end of 2008, above 800 basis points (bp), about three times the level in the previous year while the Morgan Stanley Capital International (MSCI) index fell to some 40 per cent of the level reached in 2007. With the recovery in capital flows, spreads fell and equity prices rose rapidly, but they both deteriorated after mid-2011 with the deepening of the EZ crisis. Despite some improvements in the second half of 2012, now spreads are above and the MSCI index is below the levels reached on the eve of the crisis.

The Lehman collapse and flight to safety also resulted in large drops in the currencies of most DCs against the dollar, with the notable exception of China (Chart 5). Many of them chose not to restrain the decline in view of weakened exports. Most DCs have welcomed the subsequent strong recovery in capital inflows and the boom in asset prices they helped to generate, but they have been ambivalent about their impact on exchange rates. The ultra-easy monetary policy in AEs has been widely seen as an attempt to achieve beggar-thy-neighbour competitive devaluations to boost exports to drive recovery in conditions of sluggish domestic demand. It was described as a currency war by the Brazilian Minister of Finance while the Governor of the South African Reserve Bank alluded that DCs were in effect caught in a cross fire between the ECB and the US Federal Reserve (Marcus, 2012).

DCs have responded in various ways. Initially, almost all countries had a hands-off approach to capital inflows. Many of them, notably in Asia, intervened heavily in foreign exchange markets, absorbing them in reserves and trying to sterilize interventions by issuing government and/or central bank debt. These countries avoided sharp appreciations. The total foreign exchange reserves of developing Asia increased by some $2200 billion during 2008-12 despite the decline in their overall current account surpluses. Others, particularly those pursuing inflation targeting, including Brazil, South Africa and Turkey, abstained from extensive interventions and hence experienced considerable appreciations.

There are two obvious reasons for this policy of non-intervention. First, since it is difficult to fully sterilize the impact of interventions on domestic liquidity, attempts to stabilize the currency would conflict with inflation targeting. Second, as most of these were high-interest-rate economies, sterilization would imply significant fiscal or quasi-fiscal costs, adding to government deficits and debt.

However, as upward pressures on the currencies of DCs persisted, several countries abandoned the hands-off approach to inflows and started using measures to control them. Interestingly the country that has made the most frequent recourse to such measures is Korea, a member of the Organisation for Economic Co-operation and Development (OECD) and hence is subject to provisions of its Code of Liberalization of Capital Movements (Singh, 2010). The Korean won has been one of the weakest currencies in the entire post-crisis period. Its effective exchange rate has never gone back to pre-crisis levels, eliciting remarks that, together with the UK, it is the most aggressive “currency warrior” of the past five and a half years (Ferguson, 2013). The measures of control used by Korea include ceilings on forex forward positions of banks, a levy on non-deposit liabilities and a withholding tax on interest income from foreign holdings of treasuries and monetary stabilization bonds. Korea is now launching a $15 billion stimulus plan in order to support exporters facing pressures from a weaker yen and to revive growth, the third largest after those introduced in response to the 1997 Asian crisis and the 2008 global crisis (Kim, 2013).

After 2009 several DCs started to control capital inflows, mainly through market-friendly measures rather than direct restrictions. These included unremunerated reserve requirements (URR) and taxes (Brazil taxes on portfolio inflows; Peru on foreign purchases of CB (Central Bank) paper; and Colombia URR of 40 per cent for 6 months); minimum stay or holding periods (Colombia for inward FDI; Indonesia for CB papers); special reserve requirements (RR) and taxes on banks’ positions (Brazil RR on short positions and tax on short positions in forex derivatives; Indonesia RR for total foreign assets; Peru higher RR on non-resident local currency deposits); taxes and restrictions over borrowing abroad (India on corporate borrowing; Indonesia on bank borrowing; Peru additional capital requirements for forex credit exposure); and taxes on foreign earnings on financial assets (Thailand withholding tax on interest income and capital gains from domestic bonds). Some DCs such as South Africa liberalized outflows by residents in order to relieve the upward pressure on the currency.

These measures have been designed not so much to prevent financial fragility as to avoid currency appreciations and deterioration of the current account. As noted, not only have most emerging economies welcomed the boom in asset markets, but they have also ignored the build-up of vulnerability resulting from increased corporate borrowing abroad. However, the measures have not been very effective in limiting the volume of inflows as exceptions were made in several areas. In many cases the composition of inflows changed towards longer maturities and types of investment not covered by measures. Furthermore, taxes and other restrictions imposed were too weak to match arbitrage margins. Similar measures produced different outcomes in different countries because of differences in the implementation capacity and the sanctions attached to violation.

Although ultra-easy monetary policy has continued with full force after 2010, putting pressure on the currencies of some DCs, protests from the South became much less frequent. There are basically two reasons for it. From early 2011 most developing economies started to cool and hence the pressure of capital inflows on prices eased up. Second, the shift to domestic-demand-led growth has led to a widening of current account deficits in many major emerging economies, including Brazil, India, South Africa and Turkey, and this has increased the need for foreign capital and eased the upward pressure on currencies. Indeed, as seen in Chart 5, from mid-2011 the currencies of most of these countries started to weaken.

The so-called currency war among major AEs continues unabated. The ECB’s pledge to “do whatever it takes” to save the single currency, the announcement of Outright Monetary Transactions (OMT) and a further interest rate cut by the ECB in May 2013 to bring it down to a record low of 0.5 per cent as well as the commitment of the US Fed to continue with the QE3 until unemployment fell below 6.5 per cent or inflation rose above 2.5 per cent suggest that the ultra-easy monetary policy in the US and the EZ are here to stay for some time to come. The Bank of Japan raised the inflation target in early 2013 and started a policy of aggressive QE, leading to a significant fall of the yen against the dollar and eliciting critical remarks, including from the Bundesbank president (Ferguson, 2013). In the UK, devaluations and exports have been seen as a way out of public and private deleveraging, with the government not ruling out abandoning inflation targeting. The pound sterling has depreciated in real effective terms more than any other major currency since August 2007. The Swiss National Bank has capped its currency against the euro and has been intervening heavily in order to prevent appreciation, despite a current account surplus of over 10 per cent of GDP.

However, liquidity expansion in AEs is not likely to lead to a generalized surge in capital inflows to DCs similar to that seen before the onset of the crisis although some countries favoured by international investors may experience strong inflows. First, in most emerging economies growth has slowed down sharply compared to the previous period. Secondly, interest rates have often been cut in response, thereby narrowing short-term arbitrage margins. In any case, a renewed surge in inflows of all types, including portfolio inflows, may be welcomed by several major DCs because of widened current account deficits.

Comments Off on Passing of Dr. Gamani Corea, former South Centre Chairman

We have learnt with great sadness the news about the passing away of Dr. Gamani Corea on 3 November 2013.

Dr. Corea, a Sri Lankan, was one of the most eminent economists of the developing world, having been educated at the University of Ceylon, and the Universities of Cambridge and Oxford, and obtained his doctorate at Oxford. He had been the Permanent Secretary of the Ministry of Planning and Economic Affairs and Senior Deputy Governor of the Central Bank of Sri Lanka as well as a distinguished diplomat for his country.

He is best known as the Secretary-General of UNCTAD in 1974-84, in which capacity he led the multilateral efforts to strengthen the position of developing countries in various areas, including in commodities and other areas of trade and development, and in the efforts in establishing a new international economic order.

He was a great contributor to the cause of the South and to South-South cooperation. He played a significant part in the founding of the Group of 77 developing countries in 1964 and continued to be a great support for the G77 and China throughout the years, including during his term as Secretary General of UNCTAD. He also assisted the Non Aligned Movement (NAM) in various capacities.

Dr. Corea was a major leader in the establishment and development of the South Centre, including being a Chairperson of the Board.

Dr. Corea was a member of the South Commission (1987-1990), member of the Board of the South Centre (1995-1998), Chairman of the South Centre’s Policy and Research Committee (1998-2001) and Chairperson of the Board in 2002-2003. He provided immense intellectual and personal support to His Excellency Julius Nyerere, Chair of the South Commission and the South Centre (and former President of Tanzania) until his passing away in 1999. Dr. Corea played a leadership role in directing and supervising the work of the South Centre in the various capacities through the years.

Among his responsibilities, he chaired the South Centre’s Group of Experts on Financing for Development (2001), and prepared a paper which was submitted to the Group of 77 to assist it in its participation in the work of the Preparatory Committee for the UN Conference on Financing for Development. He has chaired the NAM Ad Hoc Advisory Group of Experts on Debt (1993-1994) and the NAM Ad Hoc Panel of Economists (1997-1998), submitting its report to the XII Non-Aligned Movement Summit held in 1998 in Durban, South Africa.

With his passing away, the developing countries have lost a great champion and the world has lost a tireless leader in fostering international cooperation. He is leaving behind a rich and valuable legacy that will continue to be of benefit for the people of the South and the world for many years to come.

The theory that major developing countries have “decoupled” their economies from those of advanced economies had been promoted by establishment institutions like the IMF. However this theory has been shown to be wrong by recent events.

Developing countries experienced exceptional GDP growth before the outbreak of the crisis, averaging at an unprecedented 7.5 per cent per annum during 2000-08 while growth in advanced economies (AEs) remained relatively weak. This was widely interpreted as decoupling of the South from the North, including by the IMF. Presumably, decoupling in this sense does not imply that the South has become economically independent of the North – something that would be far-fetched given closer global integration of developing countries (DCs). Rather, it should mean increased ability of DCs to sustain growth independent of cyclical positions of AEs by pursuing appropriate domestic policies and adjusting them to neutralize any shocks from the North.

Decoupling was discussed in Akyüz (2012). As shown by several authors cited in that paper, business cycles understood as deviations from trend or potential output continue to be highly correlated. Regarding a more fundamental question of whether there was an upward shift in the trend (potential) growth of DCs relative to AEs, it was concluded that the pre-crisis acceleration of growth in DCs was due not so much to improvements in their underlying fundamentals as to exceptionally favourable but unsustainable global economic conditions including a surge in their exports to AEs, booms in capital flows, remittances and commodity prices, largely resulting from property and consumption bubbles in the US and Europe, rapid growth of international liquidity and historically low interest rates.

In the early months of the crisis, DCs were again expected to decouple from the difficulties facing AEs. The IMF underestimated not only the depth of the crisis, but also its impact on DCs, maintaining that the dependence of growth in the South on the North had significantly weakened (IMF WEO April 2007 and WEO April 2008). After the collapse of Lehman Brothers in September 2008, the global economic environment deteriorated in all aspects that had previously supported growth in the developing world, resulting in a sharp downturn in several DCs.

However, this was soon followed by rapid recovery, starting in 2009, thanks to a strong countercyclical policy response in DCs, made possible by their improved fiscal and balance-of-payments positions during the earlier expansion. Monetary policy response to the crisis by the US and Europe also helped recovery in DCs by directing capital flows back to them after a sudden stop and sharp reversal triggered by the Lehman collapse.

The combination of the downturn in AEs and strong recovery in the South was once again interpreted as decoupling. However, the initial momentum in DCs could not be maintained. Although since 2009 conditions in global financial and commodity markets have generally remained favourable, the strong upward trend in capital flows and commodity prices has come to an end and exports to AEs have slowed considerably. Furthermore, the one-off effects of countercyclical policies in DCs have started fading and the policy space for further expansionary action has narrowed considerably.

Outside China, fiscal and payments constraints started biting in most major DCs as a result of the shift to domestic-demand-led-growth, leading to fiscal tightening. Consequently, growth in DCs declined in both 2011 and 2012 after a strong recovery in 2010. In Asia, the most dynamic developing region, in 2012 it was some 5 percentage points lower than the rate achieved before the onset of the crisis; in Latin America it was almost half of the pre-crisis rate.

The IMF has now “refined” its position on the question of decoupling, revisiting the issue in IMF WEO (October 2012: chapter 4) under “Resilience in Emerging Market and Developing Economies: Will it last?” In a quantitative analysis, lumping together more than 100 emerging market and developing economies (with per capita incomes ranging from $200 to over $20.000) and examining their evolution over the past 60 years, it has concluded that “[t]hese economies did so well during the past decade that for the first time, [they] spent more time in expansion and had smaller downturns than advanced economies. Their improved performance is explained by both good policies and a lower incidence of external and domestic shocks: better policies account for about three-fifths of their improved performance, and less-frequent shocks account for the rest.” (IMF WEO, October 2012: 129. Italics in original.)

“Good policies” that the IMF has found to have improved performancein DCs include “greater policy space (characterized by low inflation, and favourable fiscal and external positions)” created by “improved policy frameworks (countercyclical policy, inflation targeting and flexible exchange rate regimes).” No robust link could be found between structural factors including trade patterns, financial openness, capital flows and income distribution on the one hand, and the “resilience” of DCs on the other.

The Fund ignores the role of positive external shocks in stimulating growth and creating policy space in DCs, but focuses on the absence of strong adverse shocks. There is ample evidence, cited in Akyüz (2012), that improved performance of commodity-exporting DCs which account for much of the acceleration in the South after 2002 was the result of the twin booms in commodity prices and capital flows which also created space for subsequent counter-cyclical policies in response to fallouts from the global crisis. These positive shocks provide a better explanation of the exceptional performance of many DCs in the past decade than “good” orthodox policies such as inflation targeting, single-digit inflation and flexible exchange rates.

Since 2011 the IMF has been constantly over-projecting growth in emerging and developing economies. The IMF WEO (April 2011) projected 6.5 per cent growth for 2012, revised it downward to 6.1 in September 2011, to 5.7 per cent in April 2012 and 5.3 in October 2012. IMF WEO (April 2013) estimates the growth outcome for these countries at 5.1 per cent, almost 1.5 points below its original projection, and recognizes the possibility that “recent forecast disappointments are symptomatic of deeper, structural problems” (p.19), revising downward the medium-term prospects of these economies (pp. 22-23). Another IMF report estimates the average potential growth rate of DCs in the Western Hemisphere at slightly over 3 per cent, far below what is required for a genuine “rise of the South” and catch-up with AEs, and recognizes that the above-potential growth achieved during 2003-12 is not sustainable without fundamental changes (IMF, 2013).

Comments Off on Strong Spillovers from North’s Crisis to the South

Not only has the “Great Recession” led to a “Great Slowdown” in developing countries, but also their longer-term growth prospects are clouded by global structural imbalances and fragilities that culminated in the current crisis. Even if the crisis in the North is fully resolved, developing countries are likely to encounter a much less favourable international economic environment in the coming years than they did before the onset of the Great Recession, including weak and unstable growth in major advanced economies, a significant slowdown in China, higher US interest rates, stronger dollar and weaker commodity prices.

Indeed, they may even face less favourable conditions than those prevailing since the onset of the crisis, notably with respect to interest rates, capital flows and commodity prices. All these imply that there will be no more Southern tail winds.

Consequently, in order to repeat the spectacular growth they had enjoyed in the run-up to the crisis, developing countries need to improve their own fundamentals, rebalance domestic and external sources of growth and reduce dependence on foreign markets and capital.

This requires, inter alia, abandoning the Washington Consensus in practice, not just in rhetoric, and seeking strategic rather than full integration into the global economy. This article and the following articles until Page 18 address this theme.

By Yılmaz Akyüz

There have been strong spillovers from the crisis in Advanced Economies (AEs) to Developing Countries (DCs). The combination of rapid acceleration of growth in DCs and relatively weak performance of AEs before the onset of the crisis was widely interpreted as decoupling of the South from the North. Although growth in DCs fell sharply in 2009 due to contraction of exports to AEs and sudden stop of capital inflows, this was followed by a rapid recovery in 2010 thanks to a strong countercyclical policy response made possible by their improved macroeconomic conditions during the earlier expansion, while growth in AEs continued to falter. This did not only revive the decoupling hypothesis, but also several major DCs, notably China and to a lesser extent India and Brazil, came to be seen as engines of growth for the world economy, notably for smaller DCs. In the event this happened to a certain degree when a massive countercyclical investment package introduced by China in 2008-09 in response to fallouts from the crisis gave a major boost to commodity-dependent DCs. However, with continued instability and weaknesses in AEs, the structural shortcomings of developing economies, including the major DCs are exposed.

Although conditions in international financial and commodity markets have generally remained favourable since 2009, the strong upward trends in capital flows and commodity prices that had started in the first half of the 2000s have come to an end and exports of DCs to AEs have slowed considerably. Furthermore, the one-off effects of countercyclical policies in DCs have started fading and the policy space for further expansionary action has narrowed considerably. Thus, growth in most major DCs has now decelerated significantly compared to the rates achieved before the onset of the crisis. In Asia, the most dynamic developing region, growth in 2012 was some 5 percentage points below the rate achieved before the onset of the crisis; in Latin America it was almost half of the pre-crisis rate.

The longer-term growth prospects of DCs are clouded by persistent global structural imbalances and fragilities that culminated in the current crisis. The world economy is facing underconsumption because of low and declining share of wages in national income in all major AEs including the US, Germany and Japan, as well as China – countries that have a disproportionately large impact on global economic conditions (Akyüz, 2011b; Stockhammer, 2012). There has also been an increased concentration of wealth and growing inequality in the distribution of income earned on real and financial assets. Financialization, welfare state retrenchment and globalisation are the most important factors accounting for these trends. Still, until the Great Recession the threat of global deflation was avoided thanks to consumption binges and property booms driven by credit and asset bubbles in the US and a number of other AEs, particularly in Europe. Several Asian DCs, notably China, also experienced investment and property bubbles while private consumption grew strongly in many DCs elsewhere, often supported by the surge in capital flows and asset and credit bubbles (Akyüz, 2008 and 2012). This process of debt-driven expansion, in its turn, led to mounting financial fragility in the US and the EU and growing global trade imbalances, with the US acting as a locomotive to major surplus countries, Germany, Japan and China, as well as to imbalances within the Eurozone (EZ), culminating in the most serious post-war economic crisis with which the world is still grappling.

In none of the major AEs and China is there a tendency for a significant reversal of the downward trend in the share of wages in national income and a more equitable allocation of wealth so as to allow rapid economic expansion based on income-supported, as opposed to debt-driven, household spending. On the contrary the crisis has widened inequality in AEs as well as several DCs (OECD, 2013c).

In the US where the downward trend in wage share started in the 1980s, in the past two decades consumption and property booms and economic expansions were driven primarily by asset and credit bubbles – first the dot-com bubble in the 1990s and then the subprime bubble in the 2000s. The current crisis has led to a greater concentration of income and wealth. On current policies the US cannot move to wage-led or export-led growth. Rather, it may succumb to the temptation of letting the current ultra-easy monetary policy degenerate into credit and asset bubbles in order to achieve a rapid expansion, very much in the same way as its policy response to the bursting of the dot-com bubble gave rise to the sub-prime boom, while exploiting the “exorbitant privilege” it enjoys as the issuer of the dominant reserve currency and running growing external deficits.